“Change is not a gate we pass through; it is the definition of life.” (Millie Florence)

The good

Supporters of the change believe that introducing an accessible savings pot can provide salvation for those in financial crises, like the one caused by the Covid pandemic. It will help people to avoid debt and prevent people from resigning from their jobs to access the total amount of their retirement funds.

The not-so-good

Critics argue that many citizens already aren’t saving enough to retire on, and giving them access to part of their retirement savings might worsen things. There’s concern that being able to access some of your funds may lead to impulsive purchases rather than ones based on genuine necessity.

A recent survey by Just SA reveals that only 11% of South Africans over 50 feel “really confident” their savings will last if they live to 100. Alarmingly, 57% plan to rely on their children or grandchildren for support in retirement.

Does it matter to me?

It matters if you are a citizen with a pension, provident, retirement annuity, or preservation fund. If you have a provident fund and were over 55 years old on 1 March 2021, you can continue with the old system or adopt the new one.

Some older retirement annuity policies won’t need to follow the new system.

How will it work?

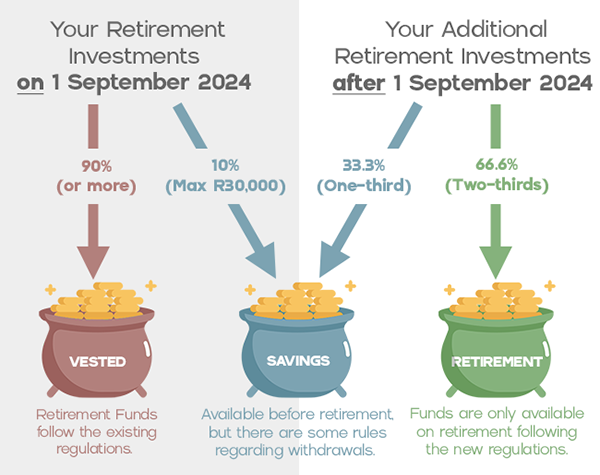

Starting 1 September 2024, retirement funds will be divided into three “pots”.

- Savings pot

- A maximum of 10% of your retirement savings, capped at R30,000, will be transferred to the savings component.

- You can use your savings (but try not to) once per tax year, with a minimum withdrawal of R2,000 and no maximum limit. Just keep in mind that withdrawals will be taxed at your marginal tax rate.

- When you reach retirement age (55), you can either add the savings pot to the retirement pot to buy an annuity or withdraw the entire amount, which will be taxed per the retirement lump sum tables.

- Retirement pot

- The retirement component will consist of two-thirds of all contributions made from 1 September onwards and is not accessible before you turn 55.

- From age 55 onwards, you must allocate the full amount in your retirement component to purchase an annuity.

- This pot may only be accessed as a cash lump sum before retirement in the event of emigration, cessation of South African tax residence (as per the current “3-year rule”), or if a non-resident member’s South African work or visitor’s visa expires.

- Vested pot

- All funds accumulated in your retirement fund up until August 31, 2024, will be ring-fenced in a separate “vested pot”. These savings will continue to be regulated by the old rules.

Here’s a visual representation of the three pots:

Tax matters

- Transfers from the savings and vested pots into the retirement pot are tax-free.

- Contributions to retirement funds will continue to be tax deductible, and there will be no tax on the growth within the fund.

- The tax deduction limits, 27.5% of annual income with a cap of R350,000, will remain the same. Contributions over these thresholds can flow only into the retirement pot. Employer contributions will still be treated as taxable fringe benefits.

The bottom line

This three-pot system marks a big step forward in retirement planning. Dividing funds into savings and retirement parts promotes thoughtful long-term planning while providing flexibility for unforeseen needs. We urge you to only dip into the savings pot as a last resort – rather try to increase your retirement investing and benefit from compounded growth.

As we near 1 September 2024, you need to take these changes on board. Please talk to us if any of the above concerns you. We’re here to help!

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© FinDotNews